How to Build Savings for the Retirement You Want

By Jane Leibbrand

When you think about retirement, will you have enough saved to maintain your current standard of living? Financial experts now recommend being ready to replace 100 percent of your income instead of 80 percent, which used to be the standard advice. Unless you plan to downsize dramatically, experts say you’ll likely spend about the same in retirement as you do now. Following are seven best practices that can help you build up your savings for the retirement you want.

Start Early

You may already be aware of one of the universal principles that virtually all financial advisors agree upon: Start saving early for your retirement. Implementing that advice can be difficult, but using creative strategies can help you clear the hurdles.

When you’re just starting out, you’re living on a beginning salary, making it hard to save any amount of money. Whether you’re single, married, or divorced, housing is usually your biggest expense. Finding ways to lower it can provide those dollars to start funding your retirement. Sharing a house or living in an upstairs or basement apartment and providing services such as lawn mowing for an older owner can dramatically lower your living expenses in your 20s when you’re entering the full-time workforce.

Delaying gratification now will pay off handsomely as your money compounds and grows in an employer-sponsored plan such as a 401(k) or 403(b). For example, if you save $3,000 a year for 10 years, starting when you’re 25, but then stop contributing when you’re 35 (not recommended), when you reach retirement age, your account would likely have about $338,000 in it, assuming your returns average 7 percent a year.

Now, let’s say you put off saving until you turn 35, and then save $3,000 a year for 30 years. By the time you reach 65, you will have set aside $90,000 of your own money, but it will grow to only about $303,000, assuming the same 7 percent annual return. That’s a substantial difference. If you’re a millennial, once you see those numbers, finding creative ways to save in your 20s makes much more sense.

Maximize All Employer Benefits

Employer-sponsored retirement plans, usually a 401(k) at private companies and a 403(b) at a nonprofit or educational institution, are the easiest ways to save for retirement. Your company handles the administrative matters while you watch your money grow.

You designate a certain amount of money that’s taken out of your salary before taxes; it automatically goes into your retirement account with each paycheck. Your money also grows tax-deferred; you don’t pay any taxes until the money is taken out years later when it’s a large nest egg.

When you participate in your employer’s plan, your company may contribute an employer match to your 401(k) or 403(b), based on a percentage of your salary—typically between 3 and 6 percent. The most prevalent scenario is a 3 percent match from your employer when you contribute 6 percent of your salary.

Or, your company may contribute a certain dollar amount—for example, $3,000 per year. Make it a point to become knowledgeable about your company’s retirement plan and benefits so you can take full advantage of them. Companies that offer a match are giving you free money.

That’s not an offer you want to pass up!

Take On Smart Debt—But Not Too Much Debt

Smart debt is an investment that has the potential to increase in value or produce income in the long-term. Purchasing a home and using government-backed student loans to complete a college or graduate-level education are good examples. Smart debt is low-interest debt; it’s also limiting debt to what you can afford to make payments on.

Make sure your budget includes reasonable housing costs that don’t keep you house-poor.

With median home prices in the Washington, D.C. metro area and other urban centers approaching $500,000, it can be difficult to invest in homeownership even on a mid-level salary. Your housing expenses should not be more than 30 percent of your gross income, or, if using the 43 percent rule, your monthly housing cost plus all of your other monthly debt payments combined should not exceed 43 percent of your gross income.

Timing can be a factor in taking on housing debt. Those who purchased homes just before the recession at inflated prices went underwater on their mortgages, with some losing their homes when their adjustable interest rates ballooned. If you plan to stay in the area for more than a few years when you purchase your home, locking in a low, fixed interest rate can save you money.

Live Within Your Means

You know how much your salary is and how much take-home pay is deposited into your bank account, but do you know how much you spend every month? Getting a handle on your spending is easier if you create and maintain a monthly budget. That way, you’ll know what you can afford in rent or for a mortgage and other expenses.

Don’t compare yourself to those living in McMansions. Pay yourself first and use automated payments to fund your retirement account. Live in the least expensive housing option available to you while you save for your future. Many millennials are heeding this advice; about 22 percent live with their parents, and in high-income areas, about 30 percent choose to do so.

Changing your spending habits can also add up to significant savings. Instead of spending $4.25 for a latte on your way to the office every day, buy an espresso or latte machine or pop in a Keurig cup and carry your own drink in the morning. That money could add up to $1,000 a year and can fund part of your retirement contribution instead of going to Starbucks.

Pay Off Your Credit Card Every Month

Another proviso on which financial advisors agree: Eliminate toxic credit card debt. It can endanger your financial health not only now, but for years to come. Pay off your credit card in full each month. If you find you can’t do it, stop using the card until your income increases, so that you’re able to do so.

You’re likely aware that credit card companies charge anywhere between 18 and 24 percent interest. If you’re in the market for a large purchase such as a furnishing a bedroom, wait until you have the money saved instead of splurging. Take on a freelance gig to make up for the amount you’re lacking. If your furniture costs $8,000 and you put it on a card with 18 percent interest and you’re making only the minimum payment, the interest you’ll pay will almost double the cost of your purchase.

Using multiple cards increases your risk for credit card debt. You may not realize how much debt you’ve incurred until the bills come in and you can’t cover them.

You’ll be rewarded financially by paying off your credit card in full when the bill comes due. This habit boosts your credit score, enabling you to garner a lower interest rate when you buy a home or a car. Your financial habits are a major factor in determining your financial health now and in retirement.

Increase Retirement Contributions as Your Salary Increases

Your salary doesn’t stay the same forever, and neither should your savings for retirement. When you receive a raise, it’s time to increase your 401(k) or 403(b) contribution. If you increase your contributions 1 percent each time your salary increases, you’ll most likely reach the maximum contribution level that the Internal Revenue Service allows. If your employer offers an auto-increase contribution, take advantage of it. That way, the increase is automatic, and you don’t have to remember to change the percentage.

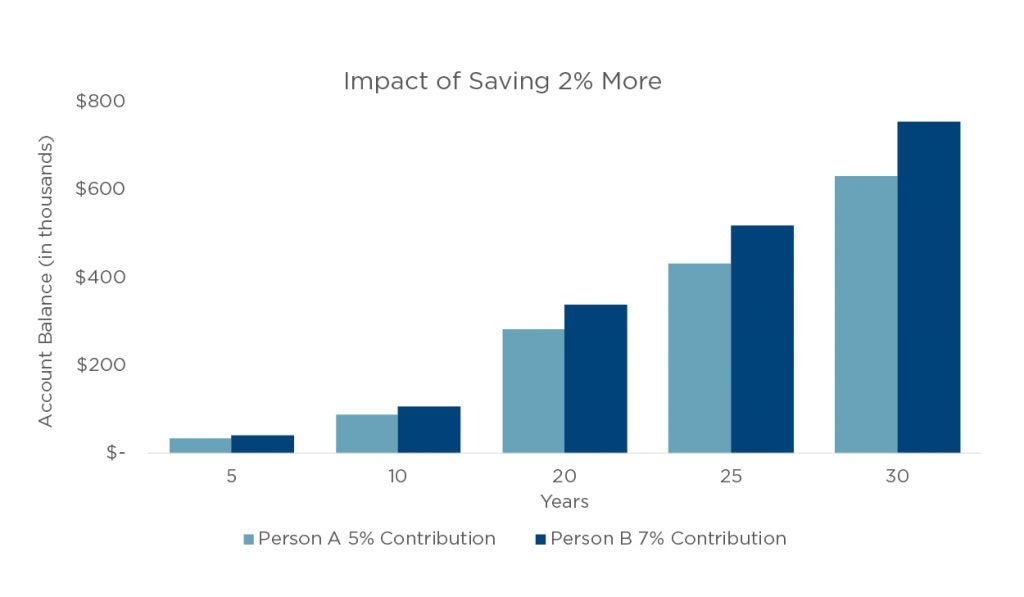

Raising the level of your retirement contributions today makes a significant difference in what you’ll have saved when you’re ready to retire. Just increasing your contribution rate from 5 percent to 7 percent could add more than $126,000 to your nest egg over 30 years, as shown in Figure Two.

Figure Two: Your Contribution Rate: A Little Extra Can Help Make a Big Difference

Source: CAPTRUST Research

Meet with Your Financial Advisor, Who’s A Fiduciary, Each Year

You make appointments with your doctors to ensure your health. Meeting annually with a financial advisor who’s a fiduciary is one of the best practices that helps you maintain financial health and build an adequate retirement fund. A fiduciary is an advisor who’s required by law to act in your best interest—not simply in the interest of the financial firm.

Using these best practices to guide your retirement savings, you’re headed for the future you want. Have questions? Need help? Call the CAPTRUST Advice Desk at 800.967.9948 or schedule an appointment with a financial counselor today.

“Ultimate Guide to Retirement“, CNN Money, 2018

Hester, Tanja “How To Save Twice Your Salary (Or More) By Age 35”, MarketWatch, 2018

Clabaugh, Jeff, “DC-area Home Values Up 40 Percent Since 2009”, Washington’s Top News, 2018

“How Much of Your Income Should You Spend on Housing?”, LendKey, 2015

Grant, Kinsey “More and More Millennials Are Living at Home With Mom and Dad”, TheStreet, 2018

Have questions? Need help? Call the CAPTRUST Advice Desk at 800.967.9948 or schedule an appointment with a retirement counselor today.