Staying the Course for Retirement

Winds of Change or Business as Usual?

Volatility has returned to the market in 2022, driven by headlines on the Russian invasion of Ukraine, rising interest rates, and fear of inflation. This comes after two years of dealing with the uncertainty of COVID-19, leaving many investors concerned about the future of their retirement accounts. While no one can say for sure how long this round of market volatility will last, times like these always provide an opportunity to reassess your goals, time horizon, short- and long-term capital needs, and level of comfort with the likelihood of continued short-term ups and downs in the financial markets.

Staying aware of your financial goals requires an understanding of where you are on your journey toward retirement. Determining your investment needs involves looking at your current age, your intended retirement age, how much you are saving, and your level of comfort as an investor.

Key Observations of the Markets

- Market volatility: It’s important to remember that periods like 2020 through 2021 are anomalies and that pullbacks of 5 to 10 percent typically happen about every year. Pullbacks of 10 percent or more have happened every three to five years. In other words, periods of volatility like the one we are currently experiencing are more the rule than the exception.

- Bond market decline: While stock markets have been grabbing the headlines, bond markets have also been hit. After 40 years of smooth sailing, investors were reminded in early 2022 that bonds are not risk free.

- Macroeconomic concerns: Investors are grappling with several macroeconomic concerns, including inflation at levels not seen in decades, the uncertain impact of the war in Ukraine, and the risk of a Fed policy mistake that over- or under-shoots the hoped-for soft economic landing without sending the economy into recession.

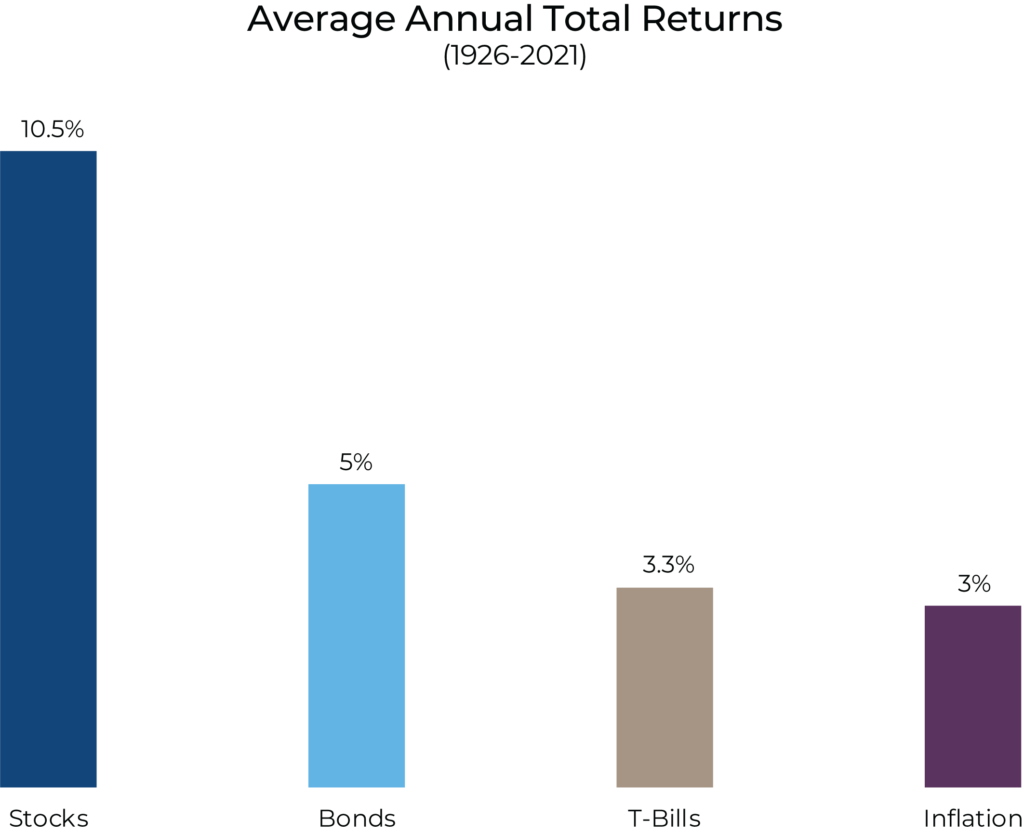

Average Annual Total Returns

As Figure One shows, over time financial markets have generated positive returns. That being said, markets do not move higher every year. During some years, markets may move up and down.

Figure One: Stocks for the Long Haul

Sources: Morningstar Direct; Ibbotson Data

For example, between January 2010 and December 2019, there were three years when stocks (as measured by the S&P 500 Index) did not appreciate, and calendar-year returns ranged from down 6 percent to up 30 percent. Despite these fluctuations, over the long term—from 1926 to 2021—stocks generated an average annualized return of about 11 percent.

Plan for the Long Term

Keeping a long-term perspective amid daily financial market noise is essential. Recent stock market performance could cause some to wonder if they should wait it out and move to the sidelines. History tells us that attempts to time the market are usually met with poor results and missed opportunities.

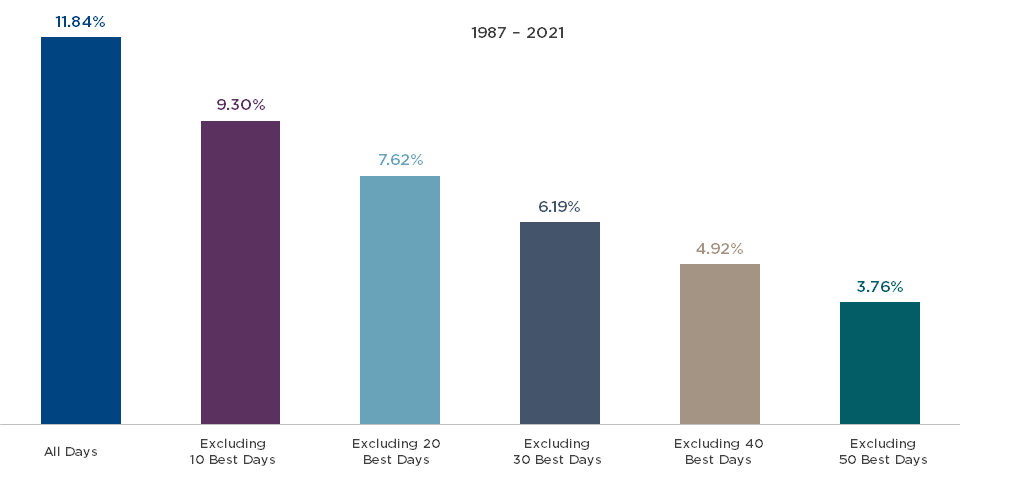

Figure Two demonstrates the folly of market timing. Investors who recognize that markets do not move in a straight line higher can benefit from staying in the market rather than trying to time short-term directional changes.

Figure Two: Time in the Market (1987 to 2021)

Looking at the S&P 500 Index (not including dividends), the annualized return from 1987 through 2021 was 11.84 percent. If you missed the ten best return days, your returns would have fallen to 9.3 percent. Missing the 30 best return days, your annualized returns would have fallen to 6.19 percent.

Finally, missing the best 50 days over this period would bring the annualized return down to 3.76 percent, a full 8.08 percentage points lower than if you had remained in the market throughout this period.

Asset Allocation Matters

A concept commonly referred to as asset allocation is a powerful tool that enables you to spread your investments among the various options in your plan based on your risk tolerance and time horizon. Studies have shown that asset allocation is the single largest driver of your portfolio’s return, significantly more important than security selection and market timing.

As Figure Three shows, asset allocation, along with adequate savings, is a key to meeting your long-term retirement goals. Proper diversification among your plan’s investment options is a critical investment concept.

Figure Three: The Power of Asset Allocation

Source: CAPTRUST Research

Weathering the Winds of Volatility

The retirement journey can be challenging, and you may occasionally feel like you need to pull up your collar and hold on to your hat. You should expect markets to fluctuate as long as economic growth remains uneven, but do not let short-term anxiety distract you from your long-term goals and objectives fostered through savings and retirement preparation. CAPTRUST is here to help you every step of the way. Your goals are our goals, and, together, we can get there. We encourage you to contact us with questions about planning for your unique retirement goals and to make sure you are not being blown off track.

Market performance illustrated here depicts historical performance by asset class using indices as a proxy and is not meant to predict future results. The information and statistics in this material are from sources believed to be reliable but are not warranted by CAPTRUST Financial Advisors to be accurate or complete.© 2022 CAPTRUST Financial Advisors.

Have questions? Need help? Call the CAPTRUST Advice Desk at 800.967.9948 or schedule an appointment with a retirement counselor today.