When Her Rise Means More Bread

By Kathleen Burns Kingsbury

Do you remember the 1960s television show Leave It to Beaver? The show featured the Cleavers, a traditional family, with dad going to work each day and mom staying home with the children. Hijinks ensued each episode with the youngest son, Theodore “Beaver” Cleaver, always getting in a sticky situation.

As with most television shows, it reflected the times in which it was made. Simply put, men earned a living and women raised children.

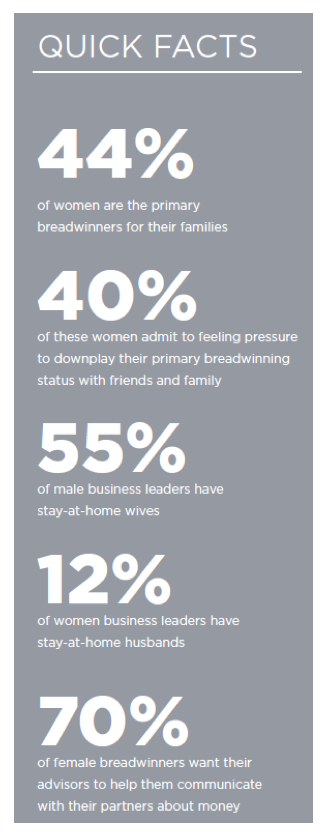

Flash forward and today 44 percent of women are the primary breadwinners in their homes, and more men are staying home and raising children than ever before. No longer is it commonplace for couples to divide economic responsibilities by gender. Instead, you and your partner get to make it up as you go along.

If you are a female breadwinner or you are married to one, you know that, at times, having the freedom to decide who does what in the family can be complicated. Questions abound. Who is going to make dinner? Who is going to pick up the kids? And how are we going to make the financial decisions? The answers require that you and your partner proactively discuss money matters on a regular basis. This can be a complex task, given that we live in a society still plagued by taboos against talking about money and filled with judgments about women who earn more than men.

Sarah knows firsthand that being the female breadwinner comes with social stigma. She always knew she would out-earn her husband Joe and that her marriage would look different from the traditional marriage her parents enjoyed. She likes working, and her income allows her husband to pursue his musical interests without the pressure of having to pay the bills. Her husband is proud and supportive of her success, but her father sees it differently. “While he doesn’t say it to me directly, I know he would prefer that I raise a family and not devote so much time to my career. But this arrangement works for us.”

It works for many couples, including Claudia and her husband, Ryan. They didn’t anticipate that she would be the primary breadwinner when they got married, but she attributes some of her success to him. “I simply began to excel in my various roles and responsibilities at work. Also, I’m more of a risk taker than my husband. I do know that I wouldn’t be where I am in my career without him.”

Whether you decided to be a female breadwinner or circumstances led you to assume this role, the key to success is proactively addressing the unique financial and emotional concerns that come with the reversal of traditional gender roles. By engaging in these meaningful conversations, you can reduce the amount of financial conflict in your marriage and model healthy money-talk skills to the next generation.

How do you begin this conversation, and what should you discuss? Here are a few ideas to get the dialogue started.

Financial Roles and Responsibilities

Historically, wives deferred all financial decisions to the husband. Today, most couples practice a “divide and conquer” strategy, in which each partner takes on some financial tasks. For example,

Sarah sets up the family budget and pays all the monthly bills. Her husband, Joe, earns substantially less, and his income goes into their vacation savings account. Together, they decide on how to invest their money, and she puts some of her earnings into a special account to fund Joe’s creative pursuits.

Claudia and Ryan take a different approach. They maintain separate checking accounts and pay bills individually. Claudia pays the mortgage, and Ryan covers the cable and utility bills. As she shares, “We have never comingled our money, and this works very well. We rarely argue about money.”

When deciding how to assign financial roles and responsibilities, consider your collective skills and knowledge base, time available to devote to each task, and how each of you might feel should one of you take the lead when it comes to managing the family’s money. Determine what system works best for your relationship now,

and keep the lines of communication open so you can adjust over time.

Division of Labor

No matter who earns the majority of the income, childcare and housework are two topics that often cause conflict in a marriage. This is especially true when the wife is the primary breadwinner, since many women try to do it all. But working full time, caring for children, and cleaning the house—while climbing the corporate ladder or running a business—is an unrealistic plan.

Claudia’s children are grown, but when they were younger, her husband took on most of the caregiver responsibilities. Her job required frequent business travel, and Ryan, while reluctant at first, agreed to and grew into his role as the principal parent and housekeeper. Claudia says, “Once I realized that I was not superwoman and asked for help, our marriage became stronger. And our kids were happier.”

Sarah and Joe’s situation is different, as they don’t have children. But Sarah does know what it is like to attempt to work full time and care for a home. When the couple first bought a house, she was resistant to hiring help and relied on Joe to pick up the housecleaning responsibilities. Her mistake was that she didn’t communicate this plan to him. “I assumed he would jump in and vacuum the house and do the laundry. When he didn’t, we fought. After several conversations, we decided that Ryan would take care of the garden and household repairs, and we would hire a weekly cleaning service. It turns out this is a much better plan!”

Fight the urge to make assumptions, and instead discuss how the household chores will get done and, if applicable, how you will parent. When it comes to routine chores, consider hiring help. Talk about the logistics, but also discuss your feelings about letting go of duties that traditionally were considered masculine or feminine. This will help each of you understand the other‘s perspective and allow you to devise a strategy that is appropriate for your family.

Dining Out

While the number of female breadwinners is on the rise, societal norms and expectations have been slow to change. When dining out, it is still customary for the waiter to put the restaurant check in front of the man at the table. The underlying belief is that men should pay for dinner. Some couples are comfortable with this ritual, while others argue about how to handle money in public.

In the past, Claudia and Ryan would fight almost every time they went out to eat with friends. While Claudia had no problem picking up and paying the check, doing so made Ryan uncomfortable. Eventually, they discussed their feelings about this societal standard and agreed that, when dining with others, Ryan would settle the tab with their joint credit card. At the end of the month, Claudia pays the credit card bill from her salary. “It is nice to no longer anticipate an argument after a nice night out on the town,” she explains.

It is important to find out how your partner feels when faced with a financial situation where the man is expected to pay. Don’t judge your partner’s emotional reaction; instead, try to put yourself in his shoes and understand his viewpoint. Remember, for centuries men have been expected to be the providers for their families, and your partner may prefer holding onto that role when conducting financial transactions in public.

With the increase in female breadwinners comes a unique opportunity for couples to create a new paradigm. No longer do you and your partner have to adhere to traditional financial gender roles if they don’t meet your needs. Instead, you can design a system that works for you, your partner, and your family. And the best way to begin this process is letting go of money silence and having a meaningful financial dialogue.

Prudential, “Financial Experience and Behaviors Among Women”, 2014.

O’Connor, Eileen, and HeatherEttinger, “Women and Wealth: What Do Female Breadwinners Want?”, 2015.

Fairchild, Caroline, “The rise of stay-at-home dads? For female execs, not so much”, 2014.

Have questions? Need help? Call the CAPTRUST Advice Desk at 800.967.9948, or schedule an appointment with a retirement counselor today.